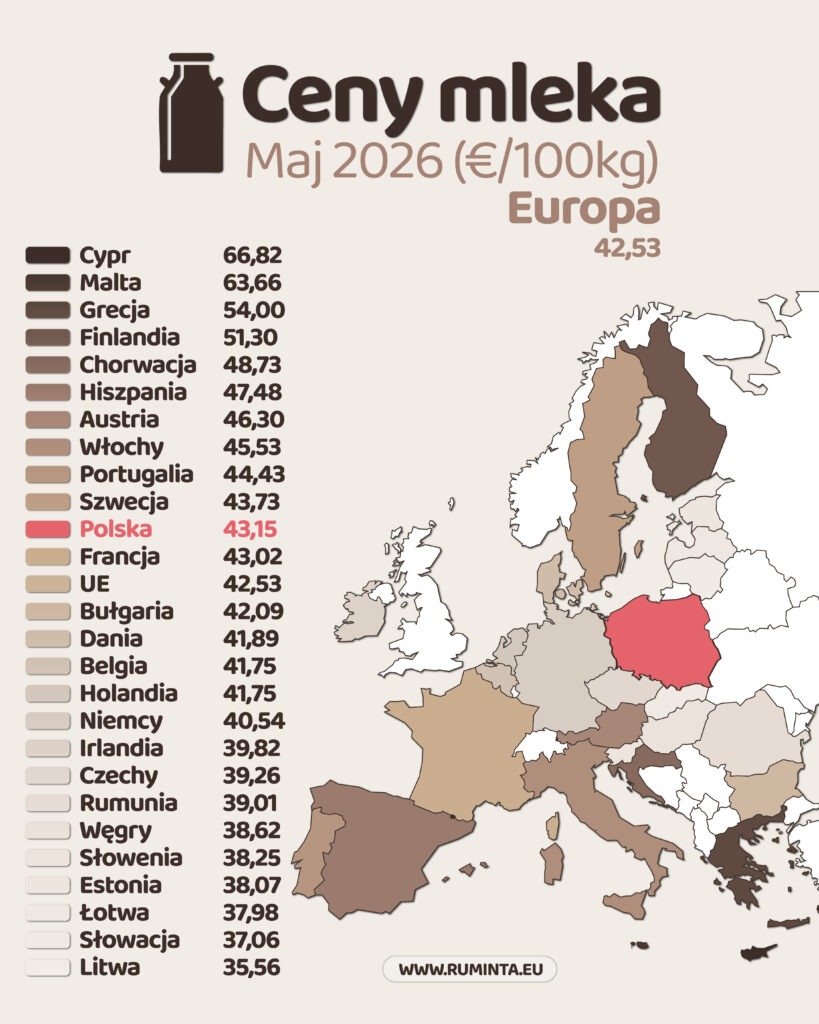

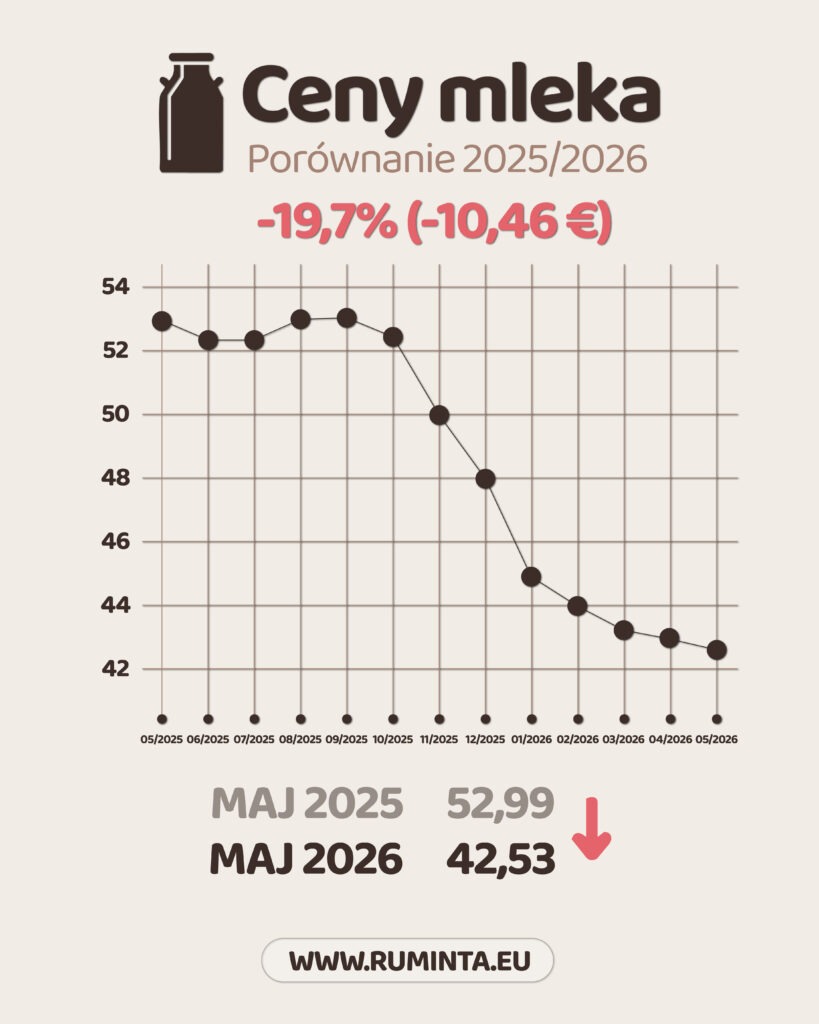

May 2026 brought another monthly drop in the average EU raw milk price. Data from the Milk Market Observatory indicates a price 42.53 €/100 kg for EU-27 (excluding Great Britain) – about 0.6% less than in April 2026 and up to 19.7% below May 2025In absolute numbers, this means a decrease of 10.46 €/100 kg compared to the previous year – an amount that for most producers translates into a very real and severe difference in revenues.

Current prices – who rules the European market?

The top of the table is still dominated by Cyprus (€66.82/100 kg) – a country that has been operating in a completely different pricing environment than the rest of Europe for years, which is due to its geographical isolation and the specificity of the local market. It is followed by Malta (€63.66) and Greece (54,00 €).

An interesting change in the May ranking is the advancement Finland to 4th place (€51.30) and a high position Croatia (48.73 €) and Spain (€47.48). These are the countries that defend their price levels more effectively than others in the face of pan-European pressure.

At the opposite extreme were Lithuania (€35.56) – the only EU country below €36/100 kg – and Slovakia (37.06 €) and Latvia (€37.98). The Baltic and Central European countries with a strong export orientation continue to bear the highest costs of the current market correction.

Poland – above average, but under pressure

Polish milk producers will receive in May 2026 43.15 €/100 kg, which places Poland on 11th place in the EU ranking – above average (€42.53). This is good news compared to the region: Germany pays €40.54, the Czech Republic €39.26, Slovakia only €37.06.

However, it is worth remembering the annual context. As recently as May 2025, the Polish purchase price was 46.04 €/100 kg – the current level means a decrease of almost 6,5% year on year. This is less than the European average (-19.7%), which demonstrates the relative resilience of the Polish market, but for producers the difference in revenue is still noticeable.

Month-to-month comparison – rate of decline

May saw a decline of 0.61 TP3T compared to April – slightly more than the previous month (-0.31 TP3T), but still a far cry from the dramatic declines seen in the autumn (October-November 2025: -4.41 TP3T). The market is slowing, though not stopping. It's worth noting that several countries saw growth or stabilization in May: Austria (+€0.46), Portugal (+€0.93), and Denmark (+€1.88) – signals that not all markets are following the same trajectory.

Year-on-year comparison – deep correction

Year on year the picture is clear: the European milk market is much weaker than in 2025. The biggest declines affected Lithuania and Denmark (-28%), Belgium (-27%) and Germany, Hungary and the Netherlands (-25%). Poland, with a decline of -19.7%, is exactly at the level of the EU average.

The exceptions are Cyprus (+1%) i Malta (+5%) – the only countries with a positive year-on-year result – and Finland and Croatia, which almost maintained the 2025 levels.

Conclusions and predictions – what next?

Several factors will be key to price development in the coming months:

Firstly, the end of the spring seasonMay and June are traditionally the peak of milk production in Europe (flush season). As cows return from fresh pastures and production begins to naturally decline, supply pressure should ease. This historically supports prices in the second half of the year.

Secondly, situation on global marketsDemand for dairy products from China and other Asian markets remains a key factor. Any recovery in imports could quickly translate into higher EU farm gate prices.

Thirdly, production costsWith current farm gate prices, the profitability of many dairy farms in Europe is under serious pressure. This could result in reduced herd numbers and reduced production – which, in turn, would naturally support prices in the medium term.

Cautious optimism seems justified: the market is no longer declining as sharply as it did in the fall of 2025, and seasonal supply factors should support stabilization or a slight rebound in the second half of 2026. Data for June and July will be key to confirming this scenario.

Follow our blog – we will keep you updated on further readings.

Check out Rumint's offer® and stay one step ahead of problems 🐮