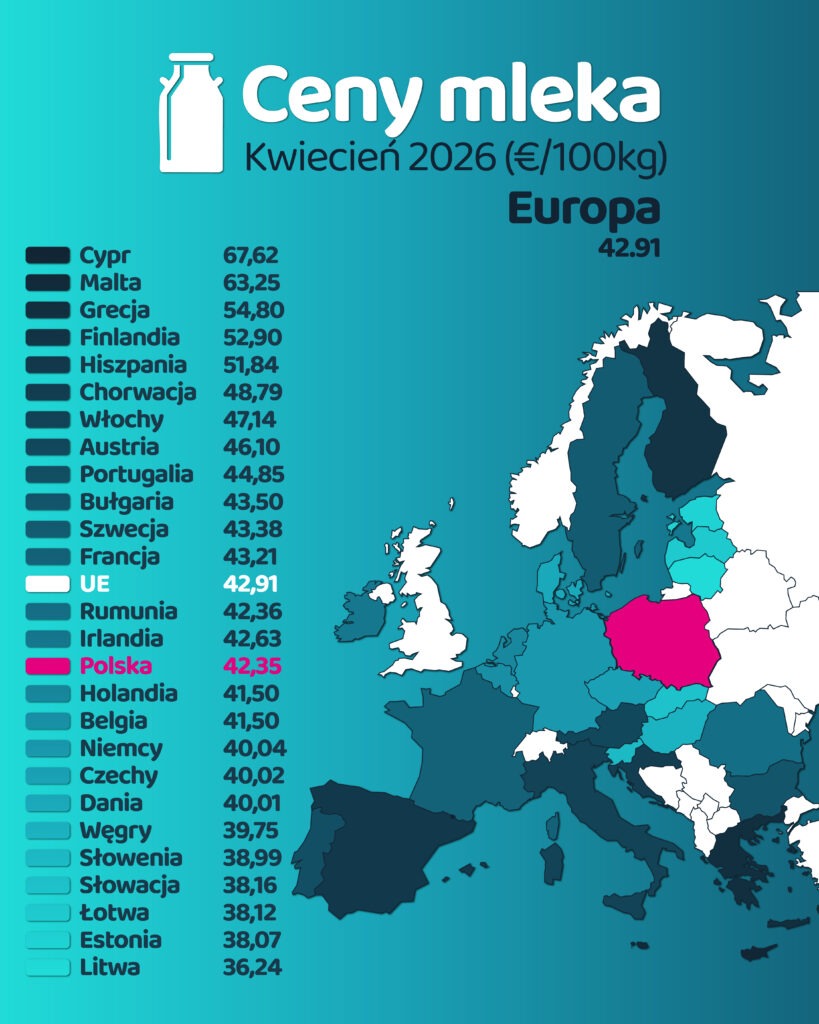

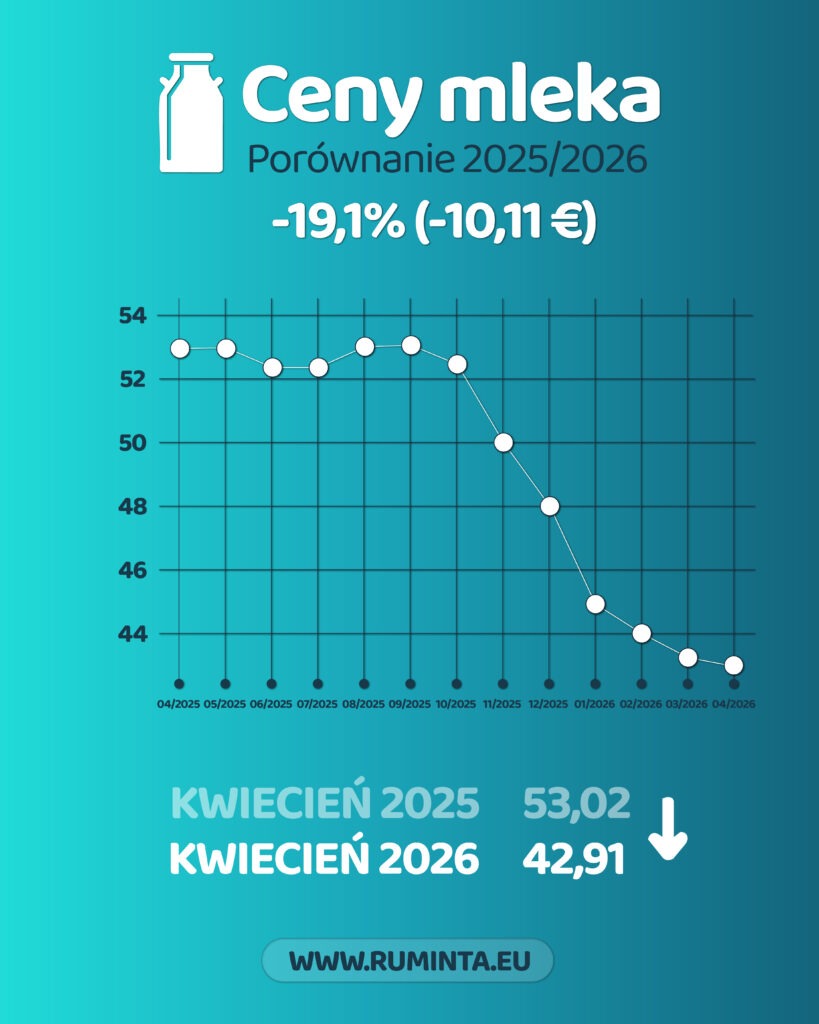

The latest Milk Market Observatory data for April 2026 confirm that the European raw milk market remains under significant pressure. The EU-27 weighted average (excluding the UK) stands at €42.91/100 kg – down 0.4% month-on-month and a substantial 19.1% below April 2025 levels. This ranks among the deepest year-on-year corrections in recent years.

Price leaders – islands and Southern Europe hold firm

Cyprus continues to lead the EU ranking at €67.62/100 kg, nearly 58% above the EU average. Malta follows at €63.25, with Greece in third at €54.80. These markets benefit from geographical isolation, limited import competition and strong local demand – factors that insulate producers from the broader European downturn.

Also comfortably above the EU average: Finland (€52.90), Spain (€51.84), Croatia (€48.79), Italy (€47.14), Austria (€46.10) and Portugal (€44.85).

Poland slips below the EU average

This is a notable development. Polish producers receive €42.35/100 kg in April 2026, placing Poland 15th in the ranking – just below the EU average of €42.91. Compared to April 2025 (€53.02), that represents a decline of nearly 20%. A trend worth watching closely.

The bottom of the table – Baltic states remain under pressure

The lowest prices are recorded in Lithuania (€36.24), Estonia (€38.07) and Latvia (€38.12). Export-oriented production structures and the continued closure of Eastern markets keep prices at the lower end of the EU spectrum.

Is the decline finally slowing?

A -0.4% monthly change is markedly calmer than the -4% to -6% drops recorded in autumn 2025. The spring flush season is adding supply, but the impact appears milder than feared. Whether this signals genuine stabilisation or a temporary pause will become clearer with May and June data.

Follow our blog and let us know in the comments – how are current price levels shaping your business decisions?