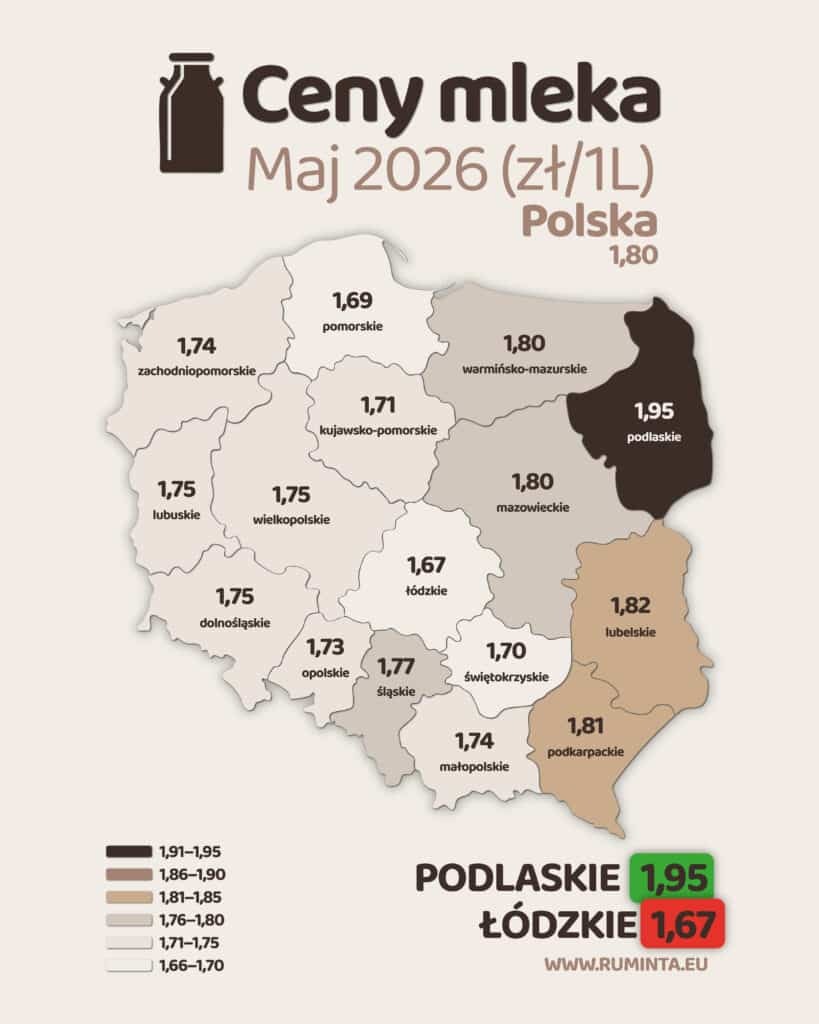

The latest data shows that May purchase prices of cow's milk in Poland continue the downward trend that has been ongoing since January 2026. The national average is 1.80 PLN/liter (180.42 PLN/hl) – a decrease of 1.2% compared to April and up to 20.0% below May 2025 level (2.26 PLN/liter). On an annual basis, this means a difference 0.45 PLN on each liter of milk – an amount that translates into a real, painful decline in revenue for an average household.

Regional diversity – Podlaskie is still the leader

The highest prices have been recorded consistently for months. Podlaskie Voivodeship – 1.95 PLN/liter, which is over 8% above the national average. This is the result of a strong concentration of large, specialized dairy farms and a well-developed purchasing and processing infrastructure in the region. Next in line were Lublin Voivodeship (1.82 PLN/l) and Subcarpathian Voivodeship (1.81 PLN/l).

At the opposite extreme remains Lodz Voivodeship with price 1.67 PLN/liter – the lowest in the country. Not much higher are Pomeranian Voivodeship (1.69 PLN/l) and Świętokrzyskie (1.70 PLN/l).

The range between the most expensive and cheapest region is 0.28 PLN/liter, or over 16% difference in the price paid to producers – within a single, common national market. This demonstrates the significant role played by local infrastructure, farm structure, and the strength of processors in a given region.

Month-to-month comparison – the pace of decline is accelerating

The month-on-month decline of 1.21 TP3T is significantly deeper than in April (-0.31 TP3T) and March (-1.71 TP3T according to earlier data). This signals that the supply pressure typical of the spring (flush) season is still strongly impacting the domestic market, more so than expected just a month ago.

Year-on-year comparison – deep correction continues

The year-on-year decline of -20.0% puts Poland in a difficult position compared to other European countries – for comparison, the EU average in May 2026 fell by 19.7% year-on-year, an almost identical figure. The Polish milk market is therefore closely following the pan-European price correction trend, without any clear signs of the resilience observed in previous months.

Conclusions and predictions

Several factors will be key to how the situation develops:

Firstly, the end of the spring seasonMay and June are historically peak milk production months in Poland and Europe. As cows transition from intensive grazing to the more stable summer production mode, milk supply should begin to naturally decrease, which traditionally supports prices in the second half of the year.

Secondly, cost pressure on farmsAt current procurement prices, the profitability of many dairy producers in Poland is under serious pressure. This could result in a reduction in herd size in some regions, which would limit supply and support prices in the medium term.

Thirdly, export and global situationForeign demand for Polish dairy products – especially in Asian markets – will have a significant impact on whether domestic purchase prices begin to stabilize in the third quarter.

Despite the challenging May reading, there is reason for cautious optimism: the approaching end of the high supply season is a natural mechanism that has repeatedly supported price rebounds in the summer and fall in the past. June and July will be crucial in confirming whether this scenario will also materialize in 2026.

Follow our blog – we regularly update data and analyze the market situation. Let us know in the comments what the purchase prices are like in your region and whether they align with the Central Statistical Office (GUS) data!